Iran's Crypto Off-Ramp Is Beijing

How the weaponisation of Western finance is building the alternative financial system that will outlast it

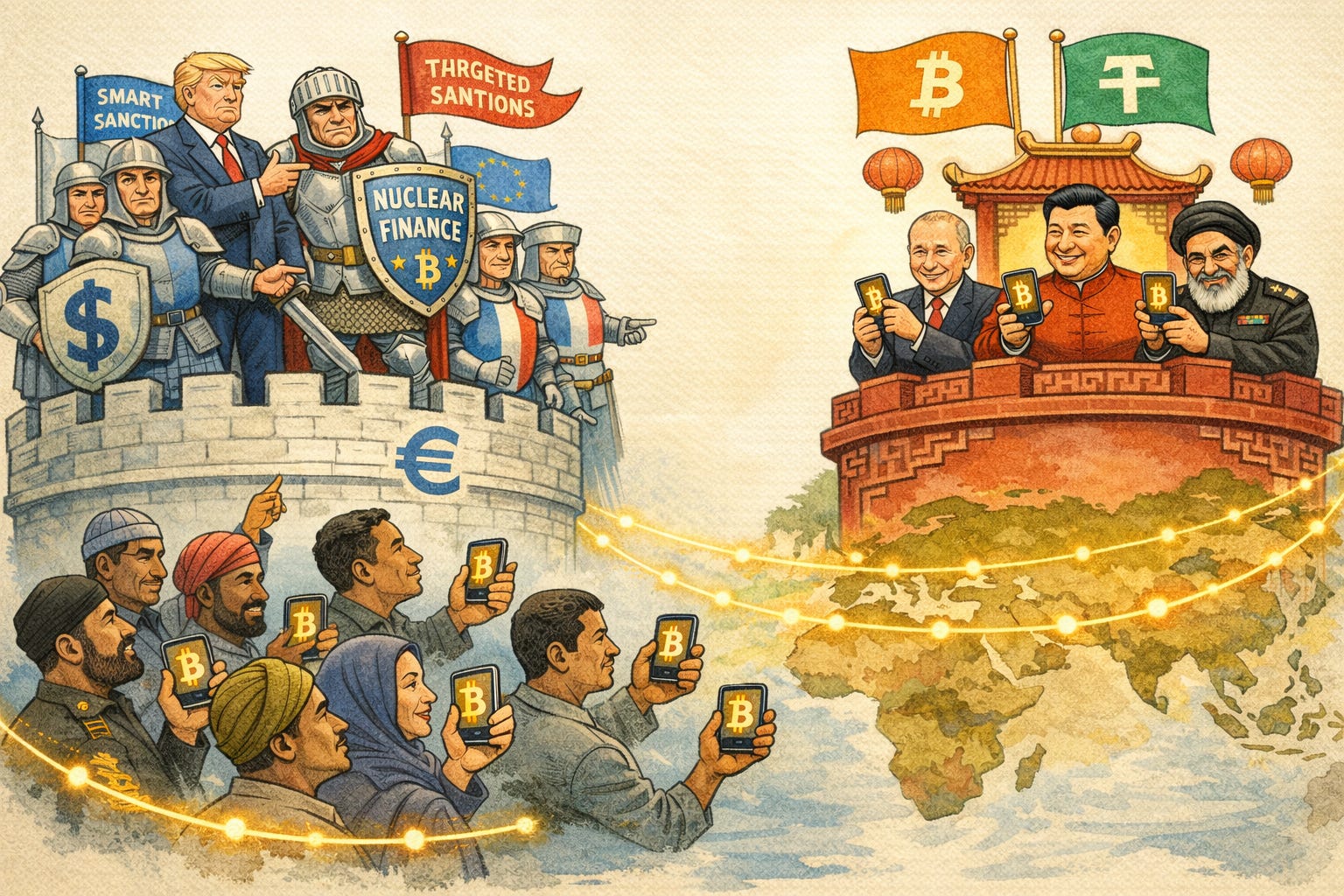

The Treasury secretary’s words were chosen for maximum effect. Scott Bessent, standing in the White House briefing room on Wednesday 16 April 2026, promised that the United States would deliver the “financial equivalent” of the bombing campaign against Iran: a cascade of secondary sanctions aimed at any bank, company, or country that …